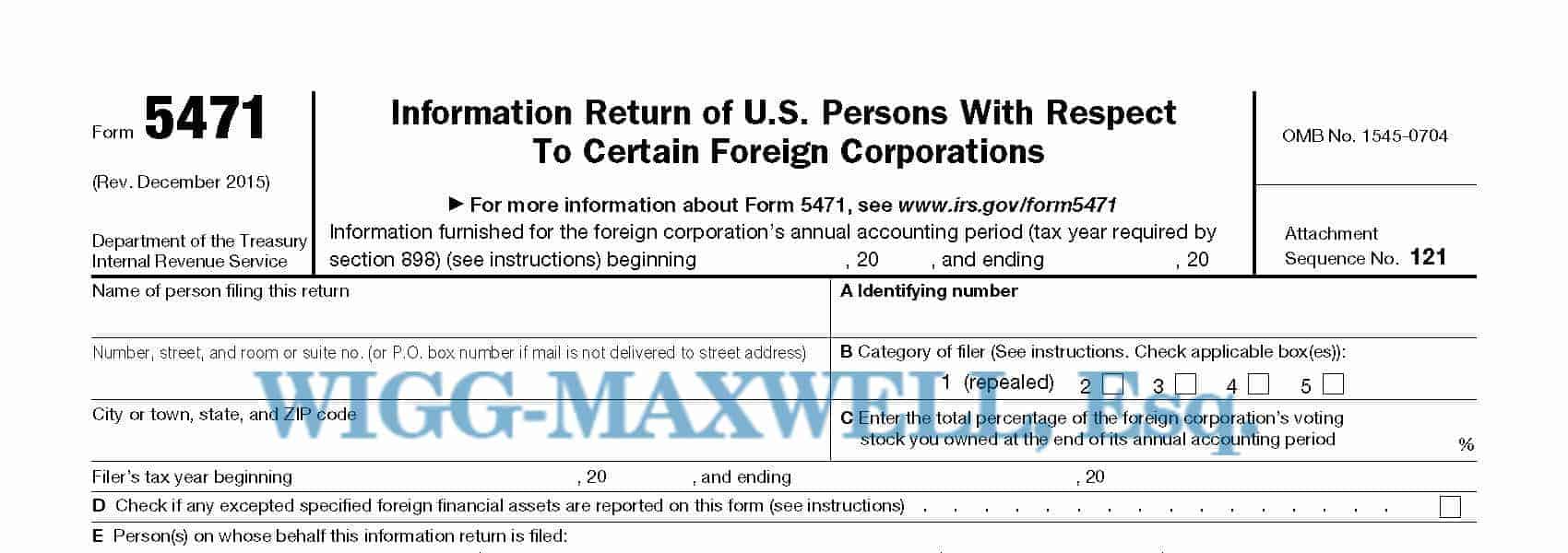

Generally companies and individuals required to file Form 5471 are subject to the current income inclusion rules for Subpart F income earned by the foreign corporation, whether the earnings are distributed by the foreign corporation or retained.

Calculating the amount of the earnings to be included in the U.S. shareholders income requires an understanding of Subpart F and an accounting for the foreign corporations earnings both in the current year and for all prior years in which the foreign corporation is treated as a controlled foreign corporation.

The accounting may particularly difficult to create. Accounting rules vary from country to country. Although the AICPA is working to encourage the IRS to accept IFRS statements in lieu of U.S. GAAP, the IRS is still requiring the accounting to be according to U.S. GAAP. This will generally require someone familiar with both accounting systems to translate the local accounting records for U.S. purposes.

Main

Chatham NJ, 07928

Phone: 973 - 507 - 9760

Email: Paul@wiggmax.com

Request Free Consultation